Changes to the Brightline tax rule from 1 July

6 June 2024

The Brightline rule refers to a tax on capital gains from residential property sold within a certain timeframe. It most often applies to investment properties rather than the main home.

From 1 July 2024, the Brightline tax will only apply to a property sold within two years of purchase. This means that a property purchased before July 2022 will not be subject to the Brightline rule. Exemptions will continue for primary residences (main home), separation or relationship property transfers, certain transfers to trusts, and inheritances.

If you’re looking to buy or sell a property and unsure if the Brightline rule will apply to your situation, get in touch with us and we’ll help you understand how these changes will affect you.

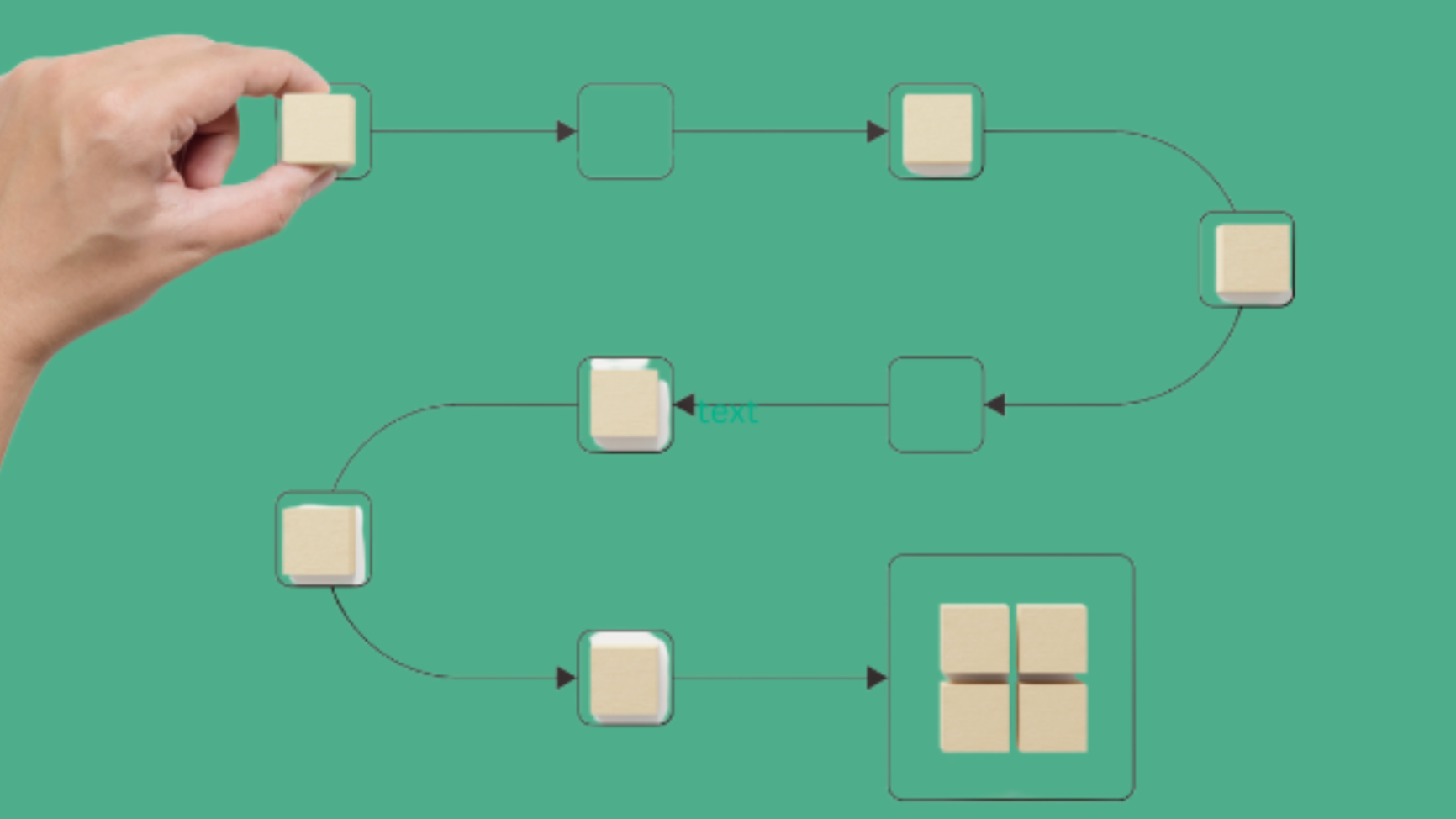

E-invoicing is becoming more and more popular in New Zealand and Australia. E-invoicing is where you deliver an e-invoice directly into your customers accounting software without it needing to be emailed to the customer. E-invoicing has a number of benefits, and best of all, you don’t need to be using the same accounting software as your customers. E-Invoicing allows you to: Streamline payments which improves your cash flow Eliminate data entry errors Reduce admin which saves time and money Enhance security as invoices are sent directly between trusted networks which means they can’t be intercepted and altered. The Government is already making moves to e-Invoicing. From 1 January 2026, any government agency which processes over 2,000 domestic invoices annually must use e-invoicing and pay 95% of these invoices within five business days. Back in 2019, the New Zealand and Australian governments set up the e-invoicing framework for both countries, which uses a New Zealand Business Number (NZBN) as a global ID for every business. It has been adopted by software provider including MYOB and you can e-invoice your customers, or receive e-invoices from suppliers, even if they don’t use the same platform. Start sending and receiving e-invoices You can set up e-invoicing in MYOB or we can help you set this up - just get in touch and we can help. It only takes a little bit of preparation to use e-invoicing, and once you have the hang of it, you’ll reap the benefits.

In today’s fast-changing business landscape, it’s crucial to regularly assess whether your business model remains effective. What worked a few years ago may not work now due to changes in technology, consumer behaviour, and market trends. To stay ahead, here are some key aspects to evaluate when determining if your business model is still fit for purpose. 1. Understanding Market Trends and Consumer Behaviour The first step is to assess how market trends and consumer preferences have evolved. Are your products or services still in demand? Has your industry undergone significant changes that require adaptation? For example, the rise of e-commerce and digital platforms has transformed how people shop and interact with brands. Staying informed about these shifts can help you identify both opportunities and potential risks. 2. Embracing Technological Advancements Technology is a driving force behind business evolution. New tools and innovations can enhance efficiency, improve customer experiences, and create new revenue streams. Assess whether your business is keeping up with technological advancements, such as cloud computing, automation, and data analytics. Leveraging the right technology can help you remain competitive and streamline operations. 3. Evaluating Financial Performance A strong financial foundation is essential for business sustainability. Regularly review key financial metrics like revenue growth, profit margins, and cash flow. If you notice a decline in these areas, it may be time to adjust your pricing strategy, cost structure, or revenue streams to improve profitability. A proactive financial review can help you make informed decisions before challenges escalate. 4. Listening to Customer Feedback Your customers provide valuable insights into the effectiveness of your business model. Actively seek feedback to understand their needs, preferences, and challenges. Are they satisfied with your offerings? Do they see value in your products or services? Use this input to refine your approach and enhance customer satisfaction. Building strong relationships with customers also fosters loyalty and trust. 5. Analysing the Competitive Landscape Competition is constantly evolving, with new players and innovative strategies reshaping industries. Conduct a thorough competitor analysis to see how others in your space are adapting. What are they doing differently? How can you innovate or differentiate your offerings? Understanding the competitive landscape allows you to stay relevant and find new opportunities for growth. 6. Navigating Regulatory Changes Laws and regulations can have a significant impact on your business operations. Stay informed about any new compliance requirements in your industry, such as environmental regulations, data protection laws, or sector-specific guidelines. Ensuring compliance not only helps you avoid legal risks but also strengthens your reputation and credibility. The Importance of Regular Business Model Evaluation Regularly reassessing your business model ensures it remains aligned with current market conditions and industry demands. By staying informed about trends, technology, financial health, customer expectations, competition, and regulations, you can make strategic adjustments to keep your business thriving. After all, adaptability and innovation are the keys to long-term business success.

Establishing a strong online presence is essential for small and medium-sized enterprises – whether you run a local bakery, a boutique consultancy, or a neighbourhood hardware store you need to be able to be found online. To help potential customers find you more easily, you can utilise the power of SEO (Search Engine Optimisation). Improving (aka optimising) your SEO helps your business appear in search results when people nearby search for products or services you offer. It’s like putting a spotlight on your business for local customers and making it easier for people to find your business, contact you, and visit your store or office. SEO seems like one of those buzz words and can easily be put in the ‘too-hard’ basket. However, here are some tips to help you increase your online visibility to potential customers. 1. Make the most of your Google Business Profile (GBP) You’ve probably heard of ‘Google My Business’ which is an online profile for your business. It’s now known as a Google Business profile and allows you to input information such as business hours, contact information, and images of your products or services. To make changes to your listing, simply search for your business in Google, and on the right-hand side it should come up with your business. Scroll down and click ‘Own this business’ and you’ll be asked to manage this business. If you want to go the extra mile, you can ask for reviews, share updates and offers, but this is not necessary. 2. Make sure your website is optimised for mobile devices People searching from their smartphones is becoming more popular than searching from computers and laptops, so it’s essential your website displays nicely on a mobile device. If you’re not sure, you can check by using your own mobile device and opening up your website – you’ll soon see if there’s a problem! 3. Build backlinks to your website Having high-quality links to your website (called backlinks), can boost your SEO. For example, you can get listed in an online directory, chamber of commerce, or local pages. If you sponsor an event, ask them to link the online information to your website. KEY TIP - make sure the websites that link to yours are ‘high quality’ – which means from reputable websites rather than random websites. 4. Optimise your website’s SEO When was the last time you looked at what you’re saying on your website? Are you using the common terms/names for what you’re selling? Is it easy to read, and have you included what people might search for in your descriptions? Make sure the words you’re using on your website match what people are searching for. 5. More complicated SEO efforts If you feel like you’ve mastered the above and are looking for some slightly more complicated things to try, here are some ideas: a) Ask for reviews from satisfied customers on your Google Business profile and on social media. This shows you value customer feedback. b) Promote your products or services to a local audience through paid ads using location-specific campaigns such as Google Ads or Meta Ads (Facebook & Instagram). c) Analyse and track how your website and paid advertising is performing by using Google Analytics and Google Search.